|

|

|

| Consumer World is a public service guide with over 2000 of the most useful consumer resources. |

|

SHOPPING Product Reviews Compare Prices Car Buying Catalogs Stores BARGAINS Discount Shops Computers Discount Travel $$$ Deals CONSUMER RESOURCES Directories Booklets Buying Info Health Home Reference Automobile Legal Fun MONEY Investments Money Matters Insurance Credit/Bank CONSUMER AGENCIES Federal Agencies State Agencies Intern'l Orgs. Consumer Orgs. COMPANIES Online Cust Serv Auto Mfrs. Product Info TRAVEL Air, Hotel Bed & Breakfast Destinations NEWS Scam Alerts Recalls Newspapers Mags INTERNET What's New Lists Search Engines Wonders References Computer Resources REGISTER for Newsletter Back to Homepage |

Credit card issuers established an October 1 deadline for stores to begin accepting these so-called EMV cards which help reduce credit card fraud. While the rules vary among credit card brands, generally, if a store fails to process a transaction using the new, more secure system when a chipped-card is presented, it will be bear the financial liability for any fraud losses. Previously, card issuers were responsible.

To use a chip-card, rather than swipe, shoppers insert or "dip" their credit card into a special slot in the retailer's checkout card terminal that authorizes the purchase. Chipped-cards help prevent the use of counterfeit credit cards by transmitting a unique code for each transaction.

"It's seems crazy that millions of dollars have been spent to issue chipped credit cards and to install special card readers, but shoppers' security is no better than it was before because the systems haven't been enabled yet by most retailers," commented Consumer World founder Edgar Dworsky. "It is also frustrating and confusing for shoppers who see the new terminals but don't know whether to swipe or 'dip' their credit cards."

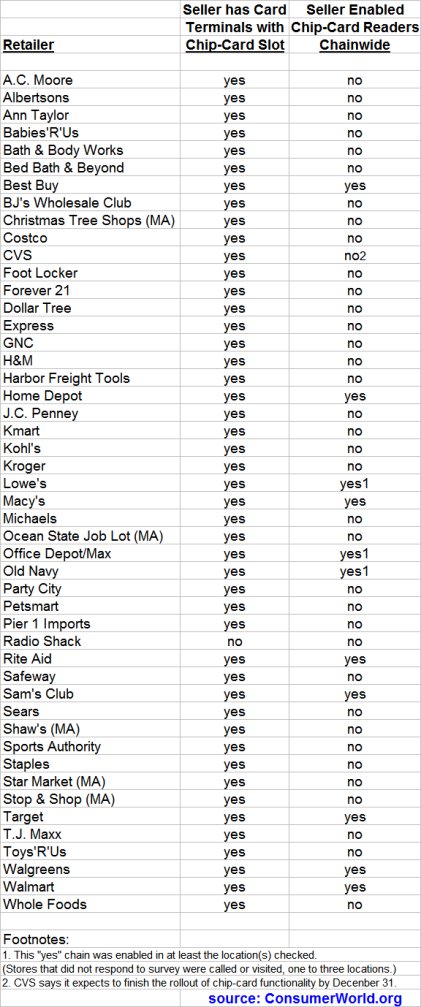

The 48 retail chains surveyed were questioned, or observed via in-store spot-checks, between December 1 - 5. All of them except Radio Shack had payment terminals equipped with card slots for chipped cards, but three-quarters of those stores didn't have them working yet. (See chart.)

Only 11 chains in the survey have enabled the system chainwide* and are processing payments using chipped-cards: Target (all stores), Walgreens (all stores), Home Depot (all stores), Rite Aid (all stores), Macy's (all stores), Best Buy (all stores), Walmart (all stores), Sam's Club (all stores), Lowe's, Old Navy, and Office Depot/Max. (* The latter three had the system enabled in at least the test stores checked but did not respond to the survey.)

Among the 75 percent of retailers that have not yet enabled the chip technology chainwide are Sears, Kmart, Costco, Michael's, Toys 'R' Us, Bed Bath & Beyond, T.J. Maxx, Marshalls, Sports Authority, Foot Locker, Whole Foods, Stop & Shop, Petsmart, Kohl's, Staples, Safeway, Kroger, and CVS (which expects full operation by the end of the year).

Why aren't stores with card-slot-equipped terminals actually using them? According to one large chain that has fully implemented the system, it is a very complicated and expensive process to get a store's system to properly interface with all the credit card networks. Others provide various reasons: they are still testing the software, stores got specifications late from some of the card networks, some card networks are slow to certify retailers' systems, stores don't want to make system changes during the busy holiday shopping season, some need to change the module inside the card-slot reader, and some say that they are only partway through rolling out the system to their stores.

In addition, there has been controversy surrounding the introduction of chipped-cards. Transactions take longer to process. Some retailers question the security provided by the new system with respect to protecting card data from hackers. And banks have been criticized for only requiring a signature rather than a more secure PIN number when using these cards. Some large retailers like Target, as well as a group of state attorneys general are urging the adoption of both "chip and PIN" when making a purchase. On the other side, some have argued that it is too difficult for shoppers using the new cards to remember to both dip them and to also enter a PIN number.

Bank industry analysts estimate that 70% of credit cards will be chip-enabled by the end of the year. Stores which have not yet updated or turned on their systems can still accept chipped credit cards the old-fashioned way -- by swiping.

as of December 1-5, 2015

======================================================== Consumer WorldÛ, launched in 1995, is a public service consumer resource guide with over 2000 links to everything "consumer" on the Internet. Edgar Dworsky, an avid bargain hunter, is the founder of Consumer World, editor of MousePrint.org an educational site devoted to exposing the fine print loopholes in advertising, and a former Assistant Attorney General in the Consumer Protection Division of the Massachusetts Attorney General's Office.

|

Just Added Here  Car Prices Find Dealers' Cost for Cars Low Rate Credit Cards 2.5Â Long Dist. No Monthly Min.++ Check Prices Find Low Prices Mortgage Rates Air Deals This weekend ++ Better Business Bureau BizRate Online stores' ratings Product Reviews Find Products by features Compare Prices What's On Sale? Lemon CheckÛ Used car histories++ Consumer Booklets Consumer Rights Home Prices Check City Sales Records |

|

Copyright © 1995-2018 Consumer WorldÛ. All rights reserved. Duplication of the collection of links herein, or any portion thereof, is strictly prohibited.

A survey by ConsumerWorld.org of four dozen national and regional retailers reveals that while virtually all have installed checkout terminals with slots to read smart credit cards with embedded computer chips, three-quarters of them have not yet enabled the technology chainwide.

A survey by ConsumerWorld.org of four dozen national and regional retailers reveals that while virtually all have installed checkout terminals with slots to read smart credit cards with embedded computer chips, three-quarters of them have not yet enabled the technology chainwide.